Key Takeaways

- The winter update of MAGNA’s “Global Ad Forecast” published Monday December 9th reveals that media owners’ ad revenues reached $933 billion in 2024, up +10%, in line with mid-year expectations.

- The advertising revenues of traditional media owners (TMO) – from the cross-platform television, radio, publishing, out-of-home, and cinema media owners – grew by an estimated +4% to $274 billion – the best performance in 14 years (if we exclude the post-COVID recovery of 2021).

- TMO ad sales were boosted by a record number of cyclical events (elections in the US, Mexico, and India, as well as the Summer Olympics, Football Euro, Copa America competitions) and a +12% growth in TMO’s non-linear ad sales (e.g. ad-supported streaming +18%) that now account for 25% of total TMO ad revenues.

- The advertising sales of Digital Pure Players (DPP) (Search, Retail, Social, Short-Form Digital Video) increased by +13% to reach $659 billion, driven by Search/Commerce ad formats (+12%) Short-Form Video (+12%) and Social Media (+18%).

- DPP ad sales were boosted by organic growth factors including competition in ecommerce (e.g., Temu and Shein now targeting European consumers), the rise of retail media networks ($144 billion), AI targeting and placement algorithms, and better monetization of short vertical videos in social and video apps.

- After a strong first half (global ad spend +12%), the ad market slowed in the second half (+8%). TMO ad sales slowed noticeably in Europe in the second half, while political advertising kept TMO growing in the US. DPP ad sales grew by double-digits through the year despite tougher comps in the second half.

- Among the most dynamic ad markets this year: France and the US (both +12%), India and the UK (both +11%). Growth was more subdued in Japan and Canada (both +8%), China (+7%), Germany and Australia (both +6%). The US market remained the largest with $380 billion, ahead of China ($155bn).

- CPG/FMCG, Government, Betting, and Finance were among the fastest-growing industry verticals in 2024, while Tech recovered, driven by “AI-Powered” marketing, and Travel slowed down. In 2025, MAGNA expects Auto, CPG and Tech to be dynamic, but Auto is vulnerable to trade and incentive policies.

- As the “Big Three” digital media owners (Google, Meta, Amazon) outperformed market growth in 2024 – with ad revenues growing by +11%, +22%, and +21% over 1Q-3Q resp. – their combined market share grew to 51% reach of global ad revenues, and 61% outside China.

- Looking at 2025, the stabilization of the European economy and the continued impact of organic growth drivers will keep the global ad market growing: MAGNA forecasts the global marketplace to grow by +6.1%, to approach the trillion-dollar mark ($990 billion) (DPP: +9%, TMO: -2%) while the US market grows by +4.9% to flirt with the $400bn milestone.

Vincent Létang, EVP, Global Market Research at MAGNA, and author of the report, said:

“The strong growth of advertising spending in 2024, despite a challenging economic environment, was of course driven by an unusually high number of major cyclical events but, more fundamentally, media innovation is what attracts a growing share of marketing budgets into advertising formats. Digital Pure-Play ad formats (Search, Retail Search, Social and Short-Form Video) are fueled by the rise of Commerce Media redirecting billions of dollars from trade marketing into digital formats. The growing reach of ad-supported CTV streaming makes cross-platform long-form video more attractive to advertisers as it now offers scale on top of addressability and brand safety. With no major cyclical drivers in 2025, MAGNA expects ad spend growth rates to slow, but the organic factors will remain at work, stabilizing TMO ad revenues, and growing DPP ad sales.”

Market Overview: Organic and Cyclical Factors Combine to Generate Historically Strong Growth in 2024

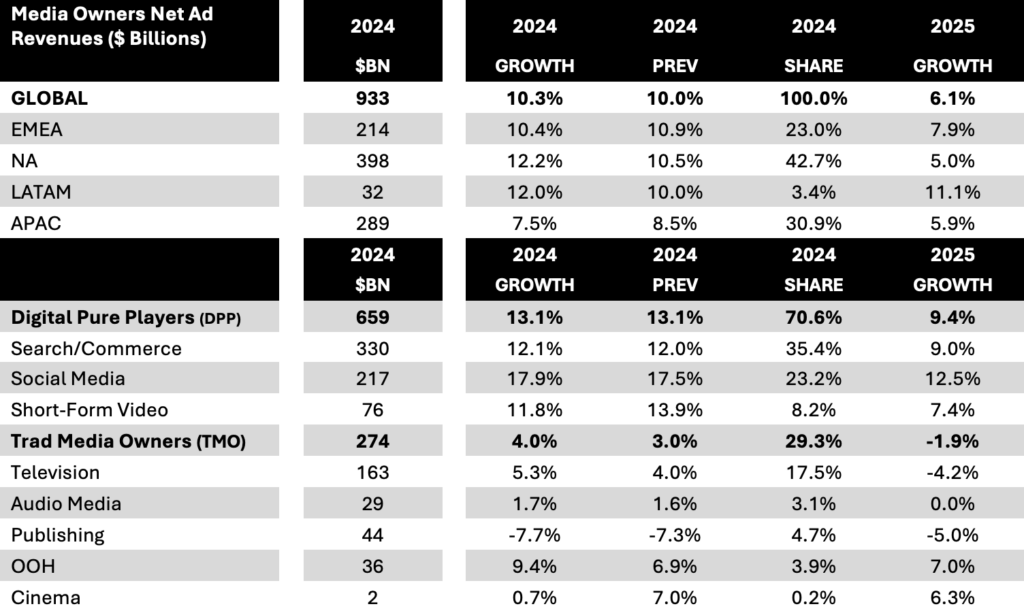

The winter update of MAGNA’s “Global Ad Forecast” reveals that media owners’ net advertising revenues (NAR) reached $933 billion in 2024, growing +10.3% over 2023. This is in line with MAGNA’s mid-year prediction (+10.0%) and a significant acceleration on the global growth recorded in 2023 (+6.4%). +10.3% is the strongest growth rate observed by MAGNA in 25 years (excluding the post-COVID surge in 2021 of +23%).

Why such strong growth in a rather lukewarm economic climate?

The exceptional number of cyclical events (including elections in India, Mexico and the US, Paris Olympics, UEFA Euro 2024, Copa América hosted by the US) were a factor, but MAGNA believes that excluding the incremental ad sales generated by these events the market would still have grown by +9.0%. The other – and main – growth factor is therefore to be found in organic market drivers in four categories:

- Commerce/Retail media Drives Digital Media Spending. As more and more product categories shift from in-store towards ecommerce, brands have adjusted their marketing efforts accordingly. CPG/FMCG brands can reallocate some of the amount negotiated with major retailers in trade marketing agreements, from in-store channels towards the digital ad formats offered by retail media networks. This allows brands to grow digital ad spend significantly without having to increase total marketing budgets, or having to cannibalize lower funnel budget spent traditional media – although some brands do that too.

- Ad-supported Streaming Boosts Long-Form Video. All traditional media owners (publishers, radio, and television broadcasters) are developing non-linear ad sales successfully. The most spectacular progress in 2024 came from ad-supported streaming. The penetration, usage and ad sales of both TMO-owned platform (e.g., Peacock by NBC, Joyn by ProSiebenSat.1, ITX, and TF1+), and pure-players (Netflix, Prime Video) grew dramatically in 2024. The proportion of users subscribing to an ad-supported tier grew everywhere. In the US, it grew from 5% to 17% for Netflix, from 10% to 30% for Disney+, and from 0% to 80% for Prime Video as Amazon introduced advertising as its default tier in 10+ key markets in 2024 (US, UK, France, Germany etc.). With more scale, in addition to addressability and brand safety, ad-supported streaming is increasingly attractive to brands. Many brands and agencies are thus reallocating ad budgets from linear TV – where impressions continue to erode by -5% to -10% per year across market and demographics – to the streaming offerings of their media partners. MAGNA believes it’s a zero-sum game, and cross-platform premium long-form television, which include television and long-form streaming, is more attractive overall against the competition of other media formats.

- Artificial Intelligence. AI is organically driving the advertising markets in two ways. Directly: all Tech companies are now launching and promoting “AI-Powered” services and products to a wide audience, which increases their overall ad budgets. Indirectly: AI is being used in the ad tech ecosystem to optimize creative costs, dynamic versioning, and programmatic effectiveness, thus improving the return on investment for brands.

- Ecommerce Competition Surge. Several new DTC brands – often coming from Asia, like Temu and Shein – are aggressively challenging traditional brands (e.g., clothing brands) and established ecommerce platforms like Amazon. This is mostly a driver for digital advertising (Search and Social formats in particular) but these brands are also using traditional media and TV campaigns.

There was one additional driver in 2024 that will not apply again in 2025: the strong improvement in the monetization of short vertical videos – that have become a dominant usage on video and social apps, since mid-2023 – which contributed to strong growth for Instagram and YouTube in 2024. We are not saying that digital monetization will deteriorate in 2025, but now that this new ad format is well established and monetized, average revenue per ad view is unlikely to increase again at a similar rate.

The economic environment is expected to remain robust in 2025. According to the IMF WEO update of October 2024, global output (real GDP growth) will remain at +3.2% i.e., the same rate as 2024 and the same rate that was expected in the April update (which was the basis of our summer forecast). The outlook is a bit brighter, however, for European markets that crawled between 0% and +1% in 2024. Germany, for instance, is expected to grow by +0.8% after stagnating in 2024, and the UK is expected to accelerate from +1.1% to +1.5%. Another good sign for marketing activity is the confirmed slowdown of consumer inflation. Lower energy costs and high interest rates successfully reduced inflation in nearly all advanced economies. From +7% to +10% in 2022-2023, consumer price inflation has now slowed to +2% to +3% in Europe and North America. The IMF is expecting CPI inflation to slow down further, to +2% or less in most mature markets, which is a positive signal for marketers and consumers. Of course, one must remain aware of two risks to this economic stability scenario: a further deterioration of geopolitical tensions that could cause another energy crisis, and a revival of trade tensions caused by a rise in tariffs.

At least three of the four organic drivers mentioned for 2024 will still move the market in 2025, although driver #4 may not be quite as strong. That is why, even without macroeconomic acceleration, MAGNA expects non-cyclical ad growth to remain in high-single digits in 2025: from +9.0% in 2024 to +7.4% in 2025. Factoring in the (lack of) major cyclical events, actual media owners’ ad revenues will grow by just +6.1%, but that should be enough to flirt with the trillion-dollar mark ($990 billion).

Media: TMO Resilience and DPP Expansion

After a strong first half (+12%), the global ad market slowed slightly in the second half (+8%). Traditional Media Owners (TMO) ad sales slowed noticeably in Europe in the second half, while political advertising kept TMO growing in the US. Digital Pure Players (DPP) ad sales grew by double-digits through the year despite tougher comps in the second half.

On a full year basis, the +10.3% growth of 2024 for all media owners was the result of TMO ad revenues growing by +4.0% to $274 billion (29.4% of global ad sales) while DPP ad sales reached +13.1%.

The +4% growth for TMO in 2024 was the best performance in 14 years (if we exclude the post-COVID recovery of 2021). TMO ad sales were driven by a record number of cyclical events (elections in Mexico, South Africa, India and the US, Summer Olympics, Football Euro, Copa America) and a +12% growth in TMO’s non-linear ad sales (e.g., ad-supported streaming +18%) that now account for 25% of total TMO ad revenues. With a lack of cyclical events in 2025 MAGNA forecasts TMO’s non-cyclical ad sales to shrink by -1.8%

Cross-platform television grew by an estimated +5% to $163 billion. Non-linear ad sales grew +18% driven by ad-supported streaming. TV benefited the most from the cyclical drivers of 2024, with six billion dollars of incremental ad revenues from political advertising for local television in the US, and one billion around the Olympic games for national TV. Excluding the impact of cyclical events, global TV advertising would have been flat in 2024. Non-cyclical cross-platform TV ad sales will shrink by -1.8% in 2025 but keeping in the cyclical factor, actual ad revenues will decrease by -4.2%.

Publishing ad revenues decreased by -3% in 2024, to $44 billion despite the growth of digital ad sales, as Magazine brands fared worse than Newspapers. MAGNA forecasts publishers’ ad sales to decline by -2% in 2025. Audio Media ad revenues grew by +2% to $29 billion in 2024 as many advertisers found the media less busy and costly than television, and digital audio (e.g., podcasting) continued to grow in popularity. MAGNA expects ad revenues to be stable in 2025.

OOH was once again the most dynamic of the traditional media formats, growing by +10% to $36.2 billion. OOH now captures 13% of total TMO ad sales compared to 11% in 2019 and just 6% in 1999. OOH benefitted from major sports events, as local and global brands were keen to reach sports fans visiting Germany or France in the summer. The growing inventory of digital ad units is driving DOOH ad revenue (+18%) and attracting programmatic budgets to OOH, which now accounts for approx. 15% of DOOH spending. MAGNA forecasts +7% growth for OOH in 2025. Finally, cinema advertising was stable at $1.8 billion (+1%) due to disappointing attendance and fewer-than-usual blockbuster releases following the Hollywood strikes in 2023. Cinema advertising remains 40% smaller than pre-COVID.

The advertising sales of Digital Pure Players (DPP) (Search, Retail, Social, Short-Form Digital Video) increased by +13% to reach $659 billion, driven by Search/Commerce ad formats (+12%) Short-Form Video (+12%) and Social Media (+18%). DPP ad sales were boosted by organic growth factors including competition in ecommerce (e.g., Temu and Shein now targeting European consumers), the rise of retail media networks ($144 billion), and better monetization of short vertical videos in social and video apps. In 2025, MAGNA expects DPP to grow by +9.4% to $721bn driven by Core Search (+6%) Retail Search (+13%), Digital Video (+7%), and Social Media (+13%).

Markets: US, UK, India, and France Among the Most Dynamic

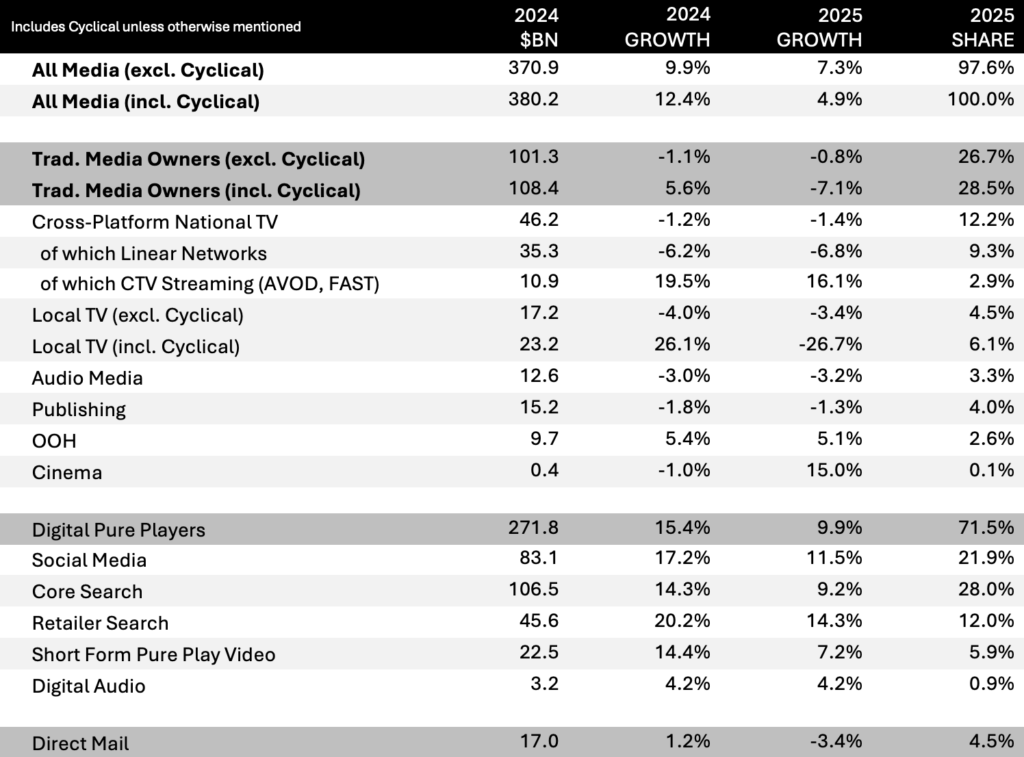

Among the most dynamic ad markets in 2024: France and the US (both +12%), India and the UK (both +11%), and Brazil (+14%). Nominal growth was much higher in a few emerging markets hit by high inflation: Argentina (+260% in local currency), Turkey (+70%), Ukraine (+26%) and Egypt (+33%). Growth was more subdued in Japan and Canada (both +8%), China (+7%), Germany and Australia (both +6%). The US ad market remains the largest by far with $380 billion this year, ahead of China ($155bn), and the UK ($54bn).

US media owners advertising revenues rose by +12.4% in 2024, to $380bn. Ten billion dollars of that came from incremental ad sales generated around cyclical events, which were the Presidential election cycle ($9.2bn of additional ad sales for local TV, digital media, and direct mail), the Summer Olympics ($1bn, national TV) and the Copa America Tournament ($60m, mostly for Spanish-speaking television). Neutralizing these cyclical dollars, the US ad market would still have grown by an impressive +9.9%. This non-cyclical growth rate was the strongest in twenty-five years if we exclude the post-COVID rebound of 2021 and was caused by a combination of digital media strength and traditional media resilience.

Digital Pure Player (DPP) ad sales rose +15.4% to $269bn (+14.8% excluding cyclical) and accounted for 70% of the total advertising market, while Traditional Media Owner (TMO) ad sales rose by +5.6% to $111bn thanks to the impact of the Presidential election and Olympic games. Non-cyclical TMO ad sales shrank by -1.1%, but that was still a resilient performance compared to previous years (e.g. -4.1% in 2023).

The most dynamic industry verticals in 2024 included Automotive (+16% across all media channels), Finance/Insurance (+15%) and Food & Beverage (+12%). Technology, which declined in 2023 and languished in the first half of 2024, finally came alive in the second half of the year as all the Big Tech companies ramped up massive ad campaigns to support their AI-Powered products, especially around the Paris Olympics.

2024 was also the year where cross-platform national television ad sales stabilized, as the growth of non-linear ad sales (mostly: ad-supported streaming) finally offset the long-term erosion of linear ad sales (broadcast and cable networks). In 2024 sales were down only -1.2%, compared to -4.3%. While linear sales dropped -6.2%, ad-supported streaming sales rose +19.5%.

In 2025, the slowdown of economic activity (real GDP growth to slow from +2.8% in 2024 to +2.2% in 2025) will slow advertising spending growth from +9.9% to +7.3%. Factoring in the (lack of) cyclical events in 2025, total media owners advertising sales will increase by +4.9% to flirt with the $400 mark ($399bn), with growth impacted by the lack of cyclical events. The US market will reach cross the $400bn mark the following year in 2026.

The US is not only the largest ad market in the world (40% of global ad spend takes place in the US), but also the most intense, as measured by the ratio of ad sales per capita: the 2024 US ratio reached $1,129, meaning advertisers collectively spend more than one thousand dollars to reach each US consumer in 2024; that’s seven times the global average ($161).

Advertisers: AI Boost Tech Marketing, Automotive in Crisis

CPG/FMCG, Government, Betting, and Finance were among the fastest-growing industry verticals in 2024, while Government & Political spending surged, Tech recovered thanks to the “AI-Powered” marketing boom, and Travel slowed down.

CPG/FMCG categories (Food, Drinks, Personal Care and Household Goods) were more dynamic in 2024 for three reasons. First, the easing in production costs removed the huge dilemma brands faced in 2022-23 (raising consumer prices to maintain profitability at the risk of consumers trading down and away from premium brands). Second, CPG/FMCG brands can grow digital advertising spending to support ecommerce sales without necessarily raising marketing budgets or cannibalizing traditional media budgets, by reallocating trade marketing agreements from below-the-line retail channels into the “retail media networks” developed by all the ecommerce platforms and traditional retailers. Finally, several CPG/FMCG brands increased their annual ad budget to associate themselves with the major sports events of 2024 on television and social media. Coca Cola came back as a sponsor in the Paris Olympics after skipping Tokyo 2021, several Beauty and Personal Care brands ran ad campaigns around superstar athletes and influencers, like Simone Biles.

Government and Political spending grew strongly in 2024 due to an exceptionally high number of elections in the world, including India, Mexico, South Africa, and the US. Political advertising is allowed on television in these markets, thus moving the ad sales needle in election years. Elections also took place in France and the UK in 2024, but political parties are not allowed to buy TV airtime and therefore elections typically don’t affect the ad market.

Auto (+9% in 2024) marketing is driven by major technological transition that spurs competition between traditional brands and newcomer electric brands, which should be enough to keep Auto as a growth category in the mid-term. Despite Government policies intended to protect domestic manufacturers, Chinese auto brands are already aggressively targeting consumers, especially in Europe: BYD was one of the main sponsors of the Euro 2024 Championship hosted by Germany – the heartland and powerhouse of the European car industry. Competition has been driving ad spend in 2024 but with the stagnation of car sales (flat in Europe and the US, with BEV down -2% in Europe), several Western Manufacturers are struggling financially. Two of the largest Auto giants, Volkswagen and Fiat/Stellantis have recently announced the reduction of production in their native countries of Germany and Italy, causing the largest social unrest in the industry in more than twenty years. As several governments look likely to cut down EV subsidies in 2025, the car market may suffer again next year, forcing auto brand to reduce marketing spending. As a result, Auto has high potential but with multiple headwinds.

Technology brands cut marketing budgets in 2022-23 due to a lack of major mass-market innovation and the need to improve profitability. Both inhibitors went away in 2024 as the revenues and profits of Big Tech soared again, and the big consumer innovation that was awaited finally came: AI. AI as a technology has been developing for years obviously, but 2024 was the year when all the big tech companies launched massive marketing campaigns around “AI-Powered” products and services, targeting both B2B audiences (e.g., Microsoft’s Copilot and IBM’s WatsonX) and BtoC targets (Meta AI, Apple Intelligence, Google’s Gemini etc.). Several Tech brands also sponsored athlete influencers during the 2024 Olympics.

Looking at 2025, MAGNA predicts that CPG/FMCG, Technology, and Finance will feature among the most dynamic industry verticals again, while Government will shrink and Auto remains a major question mark.

Media Owners: The Big Three Outperform Again

The advertising revenues of the three largest advertising vendors in the world (Google, Meta, Amazon) reaccelerated in 2023-2024 after stagnating between mid-2022 and mid-2023. Since mid-2023 and throughout 2024 Meta and YouTube have benefitted from better monetization of the fast-growing short vertical videos formats, while Amazon benefitted from CPG brands increasing lower-funnel and online marketing budgets as ecommerce sales (historically lagging in CPG) grew. Google, Meta, and Amazon reported 1Q-3Q advertising revenues up +11%, +22% and +21% respectively. As they outperform market growth, the Big Three increased their combined market share: they now account for 51% of total advertising sales globally, and 61% of ad sales outside China.

Among the top 20 media companies monitored by MAGNA, most Digital Pure Players performed well in the first three quarters of 2024 e.g., Bytedance/TikTok +20%, Apple +20%, and Snap +17%. Traditional Media Owners saw lower growth and contrasted performances: Comcast (largest TMO, driven by Olympics on NBC) +17%, Disney +6%, Warner Bros. Discovery -5%, RTL Group -8%, JCDecaux +13%.

KEY FIGURES

TABLE 1: U.S. AD FORECAST

Source: MAGNA US Ad Forecast Dec 2024. Growth rates are excluding cyclical unless otherwise mentioned.

TABLE 2: GLOBAL AD FORECASTS 2024-2025

Source: MAGNA Global Ad Forecasts, December 2024. The ad revenues of TMO include digital ad sales. All amounts in constant US dollar. PREV= June 2024 Forecast.

ABOUT THE RESEARCH

The MAGNA market research is media centric. It estimates net media owners advertising revenues based on an analysis of financial reports and data from local trade organizations; other ad market studies are based on tracking ad insertions or consolidating agency billings. The MAGNA approach provides the most accurate and comprehensive picture of the market as it captures total net media owners’ ad revenues coming from national consumer brands’ spending as well as small, local, “direct” advertisers. Forecasts are based on economic outlook and market shares dynamic. The full Ad Forecast report (80 pages) and dataset contains more granular media breakdowns and forecasts to 2028, for 70 markets.

ABOUT MAGNA

MAGNA is the leading global media investment and intelligence company. Our trusted insights, proprietary trials offerings, industry-leading negotiation and unparalleled consultative solutions deliver an actionable marketplace advantage for our clients and subscribers. We are a team of experts driven by results, integrity, and inquisitiveness. We operate across five key competencies, supporting clients and cross-functional teams through partnership, education, accountability, connectivity, and enablement. For more information, please visit https://magnaglobal.com/and follow us on LinkedIn.

MAGNA has set the industry standard for more than 60 years by predicting the future of media value. We publish more than 50 reports per year on media and advertising market trends. To access full reports and databases or to learn more about our market research services, contact [email protected].

Press Contact: Suzette Meade, IPG Mediabrands | [email protected]