ADVERTISING MARKET KEEPS GROWING THROUGH ECONOMIC UNCERTAINTY

KEY TAKEAWAYS

- The summer update of MAGNA’s “Global Ad Forecast” predicts media owners advertising revenues will grow by +9% in 2022 to $816 billion. They will grow by +6% in 2023.

- After a strong start of the year (U.S. 1Q22 +14%), advertising spending will be slowing down amidst economic uncertainty (US +8% over 2Q-4Q), but organic and cyclical growth factors will support marketing activity and advertising demand.

- Digital advertising sales will grow by +13% this year to reach 65% of total ad sales. Digital Video will be the fastest-growing ad format (+16%) followed by Search (+15%), and Social (+11%).

- The advertising revenues of traditional media companies will grow in most media: Television and Audio (both +4%), Out-of-Home (+10%), while Print advertising will decline slightly (-3%).

- Traditional media companies are deriving a growing percentage of advertising revenues from digital formats (AVOD, CTV, audio streaming, podcasting, etc). In some markets these are already contributing 10% of ad revenues in TV, 20% in audio media, and 50% in publishing, stabilizing revenues for publishers.

- Television advertising suffers from rapid erosion of linear viewing, offset by growing AVOD revenues, strong pricing in the first half, and extra spending around cyclical events (mid-terms, Olympics, FIFA World Cup).

- The U.S. ad market will grow above average (+11% to $326 billion) as it is relatively insulated from the economic consequences of the Ukraine war and is boosted by record political advertising ($7bn this year).

- The second largest ad market, China (15% of global advertising revenues), will grow below average (+8%) due to endemic difficulties (stricter regulatory environment for digital media, severe COVID lockdowns).

- Among other top 15 advertising markets the strongest growth will come from India (+15%) and South Korea (+11%) while Germany (+6%) and Italy (+3%) will suffer the most from the post-Ukraine economic environment.

Vincent Létang, EVP, Global Market Research at MAGNA and author of the report, said:

“Most of the headwinds facing the advertising market this year were expected: economic landing following a red hot 2021, continued supply issues generating inflation, and mounting privacy restrictions slowing down the growth of digital ad formats. On top of that, the war In Ukraine now exacerbates inflation and economic uncertainty. Nevertheless, MAGNA believes full-year advertising revenues will grow again in 2022 at a healthy rate, helped by a strong start to the year, on top of organic and cyclical drivers.

Organic growth factors (continued and broad-based ecommerce spending, digital marketing adoption), strong cyclical drivers (record political spending in the U.S., Winter Olympics and FIFA World Cup), and the strength of emerging or recovering industry verticals (Travel, Entertainment, Betting, Technology) will generate enough marketing demand to offset headwinds and keep the advertising economy growing in full-year 2022.”

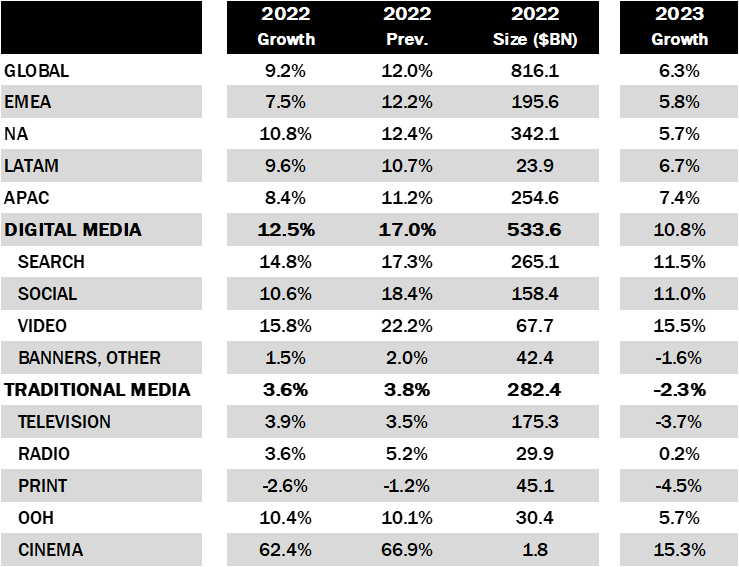

GLOBAL FORECAST: +9.2%

Globally, media owners’ advertising revenues will grow by +9.2% this year to nearly $828 billion i.e. 32% above the pre-COVID level of 2019. MAGNA was always expecting the global advertising market to slow down significantly in 2022 following the unprecedented levels of growth observed in 2021 (Global +23%, U.S. +26%) caused by a once-in-a-lifetime “planetary alignment” of factors: the V-shaped economic recovery and the marketing consequences of post-COVID lifestyles. Still, in its December 2021 update, MAGNA was expecting +12% for global, all-media advertising revenues in 2022. The reduction of our forecast from +12% to +9% is due to two main headwinds: a global economic slowdown since 2Q (full-year real GDP growth +3.6% according to IMF compared to +4.9% six months ago), and the mounting restrictions to data-driven targeting affecting digital advertising sales (e.g. the impact Apple iOS changes have had on display and social ad formats).

Nevertheless +9% in 2022 would remain above pre-COVID growth rates (average 2015-2019: +7%). The economic slowdown will really start to affect ad markets in 2Q and 3Q and MAGNA anticipates lower growth over the period 2Q-4Q, as well as throughout 2023. Nevertheless, the full-year 2022 forecast downgrade would have been much steeper if not for a stronger-than-expected first quarter recorded in most markets (+14% in the U.S.). Growth expectations would also be lower if not for the strong cyclical factors of 2022: the U.S. mid-term election (bringing almost $7 billion to local TV stations and digital media), and two global sports events: the Beijing Winter Olympics and FIFA World Cup (Qatar, November). Without cyclical ad dollars, television revenue growth would be below +2% instead of growing by +4% this year.

Offsetting the effect of a weaker economic environment, organic drivers continue to fuel marketing activity and advertising spending. Among these: the competition between brands to gain leadership in new, fast-growing product verticals driven by lifestyle or regulatory changes (e.g. sports betting, food apps, direct-to-consumer disrupters), and the growing adoption of digital advertising by both local businesses and consumer brands, often at the expense of “below-the-line” marketing channels. Most industry verticals are expected to stabilize or increase ad spend this year. Travel, Entertainment, Betting, and Technology are expected to grow the most, while Automotive and CPG/FMCG budgets may be under pressure due to supply chain and cost issues.

Around an average growth rate of +9%, MAGNA anticipates North America to grow the most (+11%) followed by LATAM (+10%), APAC (+8%) and EMEA (+7.5%).

The EMEA economy and ad markets will slow down more than other regions in 2022 because of the impact of the Ukraine war on trade and energy costs and energy supply (40% of natural gas consumed in Western Europe comes from Russia). Additional headwinds include supply chain issues and the slowdown in Chinese imports, hurting manufacturing industries, typically in Germany, or the food and luxury industries in France or Italy. In April 2022, the IMF published real GDP forecasts between +2% and +3% for most of Europe (with Spain and UK slightly higher), i.e., 1 to 2% below the IMF forecasts in October 2021, and significantly below the global average (estimated at +3.6% at the time). Finally, most European economies and ad markets are mature, with all consumer brands and many SMBs already using the full palette of advertising formats, including digital formats and programmatic technologies. Marketing activity and ad spending are therefore more vulnerable to economic slowdown than in emerging regions that are driven by organic growth in media usage and marketing usage. The U.S. ad market (40% of the global advertising revenues) will grow above average (+11% to $326 billion) as it is relatively insulated from the economic consequences of the Ukraine war and boosted by record political advertising. The second largest ad market, China (15% of global advertising revenues) will grow below average (+8%) due to endemic headwinds: a stricter and less predictable regulatory environment for digital media giants, and severe COVID lockdowns under the “zero COVID” policy. Among other top 15 advertising markets the strongest growth forecast are India (+15%) and South Korea (+11%) while Germany and Sweden (both +6%), and Italy (+3%), will suffer the most in the post-Ukraine war economic environment.

OUTLOOK BY MEDIA: THE DIGITAL LANDING

Advertising revenues of traditional media owners (TV, radio, OOH, print, cinema) will grow by +4% to $282 billion i.e. 94% of the pre-COVID market size (2019). Out-of-home will perform best with advertising revenues growing by +10% to $30 billion (already 93% of 2019 levels), followed by Audio and Television (both +4%) and Publishing (-3%). Without cyclical ad dollars, traditional media revenues would grow by just+2% instead of +4% this year. Traditional media companies are deriving a growing share of their ad revenues from digital formats (AVOD, streaming, podcasting…): in some markets these are already contributing to 10% of total TV ad sakes, 20% in audio, 50% in publishing.

Television continues to suffer from erosion of linear reach and viewing: -5% to -15% per year among adults under 50. -5% per year for the entire population. This is however offset by three drivers: (1) growing AVOD revenues (+10% to +15% this year), (2) double-digit inflation in cost-per-thousand pricing so far this year, and (3) incremental ad spend around cyclical events (mid-terms and Winter Olympics in the US, FIFA World Cup). Without cyclical dollars, television ad sales would grow by +1.6% this year, instead of +3.9%.

OOH is expected to grow by double-digits for the second year (2021: +12%, 2022: +10%, following a -25% decline in 2020) which brings it close to the pre-COVID market levels. MAGNA anticipates OOH to complete the “COVID recovery” as early as this year in the U.S., although it will take one or two more years at a global level. The OOH medium benefits from the recovery of consumer spending, and a positive industry exposure (Entertainment, Betting, Travel). The OOH industry is also reaping the benefits of its investment in technology and innovation over the last ten years; as digital OOH units reach critical mass (25% of total OOH ad sales) and omnichannel programmatic platforms can now include connected OOH screens in cross-media campaigns, OOH can tap into new and more vertical opportunities (CPG, Pharma, Retail).

Revenues from digital advertising formats (search, social, video, banners, digital audio) will reach $534 billion this year (+13%). Digital formats now represent 65% of total advertising sales worldwide. Search will remain the largest advertising format ($265 billion), ahead of Social (+11% to $158 billion), while Digital Video formats will be the most dynamic (+16% to $68 billion). All the same long-term drivers of digital advertising spending growth are in place, with consumers streaming more, spending online via ecommerce channels, and engaging with more digital media while working from home. However, there are also new headwinds, including broader economic and inflationary pressure, as well as the impact of Apple’s iOS privacy changes and impending future data collection changes that are offsetting some of that organic strength. As a result, the mix of digital spending will shift slightly in 2022 and beyond, away from social media and towards keyword formats and other campaign strategies that can directly attribute advertising spending to sales.

Digital video will be the most dynamic format in 2022 (+16% to $68 billion), reflecting the continued shift of viewing away from linear TV and towards on-demand, addressable platforms (mobile devices and, increasingly, connected TV). Long-form VOD has been mostly subscription-centric for the first ten years, but as SVOD subscription are approaching saturation, big SVOD players like Disney+ and Netflix are considering introducing cheaper, ad-supported tiers, which would bring more ad budget into digital video looking forward. Search will remain robust (+15% to $265 billion) as consumers continue to spend online, and because keyword formats are insulated from data privacy headwinds. Social media advertising sales will strongly decelerate this year to the slowest pace on record: +11% to $158 billion. This abrupt slowdown reflects difficulties attributing social platform spending to consumer purchases outside the social network walled gardens. Social’s mild slowdown will persist until in-app social commerce products are rolled out to again provide social campaigns with perfect visibility on consumer purchases.

Programmatic technologies, and audience targeting in general, remains the growth engine of many digital formats; programmatic advertising will continue to evolve as the privacy landscape matures. Changes in the data landscape moves budget from one digital format to another rather than away from digital campaigns entirely. Despite digital advertising’s slowdown in 2022, digital (and digital OOH) is still growing faster than every other format, as data and targeting help brands provide a more impactful advertising experience for consumers.

WHY SOCIAL ADVERTISING IS SUDDENLY STRUGGLING

MAGNA was always expecting social media advertising to decelerate in 2022 following explosive growth in 2021 (+36%). In the December 2021 update, MAGNA was predicting +18% in 2022 (half the growth of 2021). In this update we downgrade the 2020 growth forecast by seven percentage points to +11% – i.e. more than any other ad format. This is because social ad formats are hit by a combination of headwinds, with the last two in the list below being endemic/specific to the social ad format.

- Client saturation. In advanced mature markets, the social media budgets of consumer brands have reached a scale where any further growth comes under more financial scrutiny and becomes more vulnerable to current or anticipated business outlook. In 2020-21, millions of small businesses kick-started social media marketing during and after COVID. This is still happening in 2022, but at a slower pace.

- Audience saturation. Reach and time spent with social apps are nearly saturated in all advanced markets (Western World, China), and advertising growth in 2021 was almost entirely driven by pricing rather than volume. The plateauing in usage and ad impressions is increasingly clear this year, and incumbent players have reported declines in some mature markets.

- Targeting Restrictions: Since Mid-2021 the new Apple policy allowed millions of social media app users to opt out from sharing their device IDs and therefore prevented them from being targeted based on their data. Furthermore, it was difficult to tell what products users exposed to social media campaigns were purchasing because of that advertising spending. The impact was gradual: it started to visibly affect attractiveness and ad sales around the end of 2021, particularly for Meta and Snap.

As a result, in a social media market that is growing by only +10% or less for the time being, the rise of TikTok (already 10% market share in the U.S.) is an additional headwind for incumbent social platforms. Past a difficult 2022, when ad sales must compare with a 2021 year that was still mostly without targeting limitations, the market should stabilize or recover some strength. Additional privacy measures may come from Apple and Google in 2023 (nothing as detrimental as iOS14) but social media players will introduce other ways to become attractive again e.g. in-app social commerce, partnership with retail media networks etc.

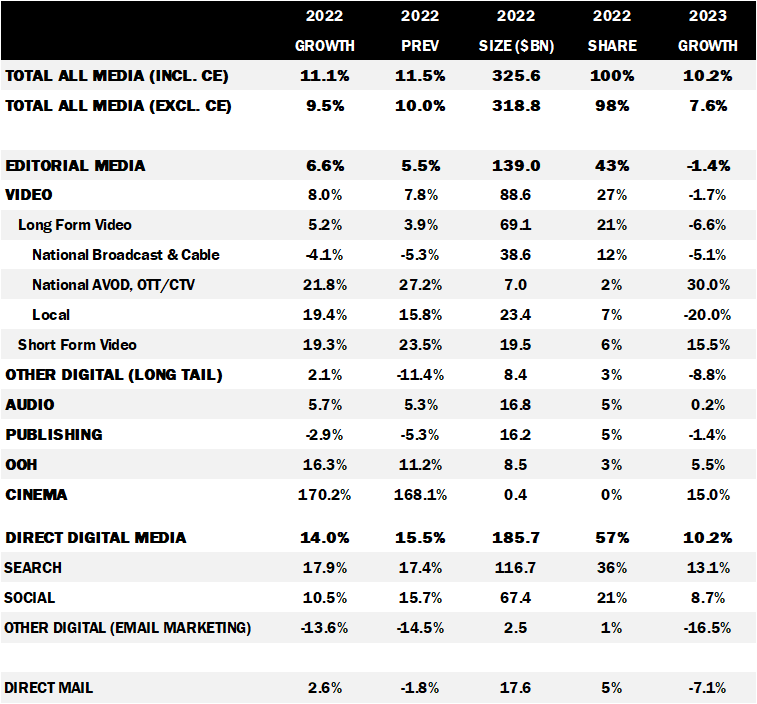

U.S. FORECAST: +11.1% TO $326 BILLION

In the U.S., Media Owners Advertising Revenue are expected to grow by 11.1% this year, to reach a new all-time high at $326 billion dollars (40% of the global advertising market), including political.

This is only slightly below MAGNA’s previous expectations for 2022 (+12.6% in March, +11.5% in December). MAGNA reduced its growth forecasts for 2Q22 to 4Q22 due to the economic slowdown, but that is partially offset by the stronger-than-expected market performance recorded in 1Q22 (+14%) and an increased forecast for political spending (now +51%).

Cross platform video advertising will grow by +8% to $89 billion as the slowdown of national linear TV (-4% to $38.6 billion) will be offset by long-form AVOD (+22% to $9.0 billion), short-form pure players (+19% to $19.5 billion) and local TV benefitting from record political spend (+19% to $23.4 billion). Cross-platform audio advertising (broadcast radio, audio streaming and podcasting) will grow by +5.7% to $16.8 billion while cross-platform publishing ad sales will shrink by -3% to $16.2 billion.

OOH sales will gain +16% to $8.5bn and surpass its 2019 pre- COVID high in 2019, one year ahead of previous expectations. Direct Mail will also benefit from political campaigns and revenues will grow by +2.6% to $17.6 billion.

Pure play digital media advertising sales (search and social media) grew by just +16% year-over-year to $42.5bn, in the first quarter of 2022, as the slowdown continues from 3Q21 (+44% yoy) and 4Q21 (+19%). Social media sales slowed to +8% in the quarter (compared to +38% in 2021) as an update in privacy restrictions set by Apple has significantly reduced growth. Conversely, search advertising remained strong in the first quarter, at +24% to $25.5bn, as interest from advertisers has shifted from social media to search in the wake of the privacy change by Apple. For the full year 2022, pure play digital advertising sales will still grow by +14% to $195bn. Search will lead performance at +18% to reach $116.7 billion, while social media will grow to $67 billion (+11%).

In terms of industry verticals, Entertainment and Travel will be among the main drivers for advertising spending growth in 2022. Both are finally recovering from a protracted COVID hangover as blockbusters and movie-goers meet in theaters again, and consumers are travelling again for pleasure or business. The streaming war may ignite again as Disney+ (this year) and Netflix (possibly next year) may launch game changing AVOD tiers. Sports Betting is becoming a major category; until local and digital media have captured the bulk of the spending, but national TV will increase its share as it is legalized in ever more states (New York this year, California and Texas possibly in 2023).

On the other hand, CPG categories (Food, Drinks, Personal Care, Off-the-Counter Pharma) may stagnate or decrease ad budgets this year. Retail sales were strong in the first four months, but supply issues and high inflation on commodities are pushing up the price of CPG products and hurting sales. The $5-a-gallon gasoline is having a disproportionate effect on the discretionary consumption of low-income families, forcing them to shop away from premium brands in CPG, tech and fashion. Automotive ad spend will likely not recover yet, as the lack of car inventory continues to be a major damp on ad budgets, only partly offset by the high-funnel campaigns for electric vehicles or online sales apps.

One bright spot however is, as usual, political advertising. Nearly $8 billion was raised by candidates and PACs, by the end April 2022, which was +85% higher than in the previous midterm cycle in 2018. As a result, MAGNA increases its forecast for full-year incremental political advertising revenues: the additional ad dollars will reach $6.7 billion this year (+51% over the 2018 tally).

Local broadcast stations local addressable ad formats (local cable, CTV) will get two thirds of the political bonanza (around $4 billion) while the third will mostly benefit pure-play digital ad formats: short-form video will reach half a billion dollars (+230% vs 2018), while social media will grow by +165%. For the first time political advertisings will account for 1% to 2% of total advertising revenues for social and video media this year.

TABLE 1: US ADVERTISING REVENUES

TABLE 2: GLOBAL ADVERTISING REVENUES

ABOUT THE RESEARCH

The MAGNA research is media centric. It monitors net media owners advertising revenues based on a bottom-up analysis of financial reports and data from media trade organizations; other ad market studies are based on tracking ad insertions or consolidating agency billings. The MAGNA approach provides the most accurate and comprehensive picture of the market as it captures total net media owners’ ad revenues coming from national consumer brands’ spending as well as small, local, “direct” advertisers. Forecasts are based on economic outlook and market shares dynamic. The full report contains more granular media breakdowns and forecasts to 2025, for 70 markets.

Next Global Forecast: December 2022 – Next US Forecast: September 2022.

ABOUT MAGNA

MAGNA is the leading global media investment and intelligence company. Our trusted insights, proprietary trials offerings, industry-leading negotiation and unparalleled consultative solutions deliver an actionable marketplace advantage for our clients and subscribers.

We are a team of experts driven by results, integrity and inquisitiveness. We operate across five key competencies, supporting clients and cross-functional teams through partnership, education, accountability, connectivity and enablement. For more information, please visit our website: https://magnaglobal.com/and follow us on LinkedIn and Twitter.

MAGNA has set the industry standard for more than 60 years by predicting the future of media value. We publish more than 40 reports per year on audience trends, media spend and market demand as well as ad effectiveness.

To access full reports and databases or to learn more about our market research services, contact [email protected].