Pre-eminent industry barometer transforms into an actionable tool for brands to evaluate responsibility of multiple media types across 150+ global partners

NEW YORK (October 13, 2022) — IPG Mediabrands and its intelligence arm MAGNA, today unveiled the 4th issue of its signature Media Responsibility Index (MRI 4.0), an initiative that strives to raise industry awareness and standards around harm reduction for brands and consumers in advertising. MRI 4.0 has transformed from an analytical study of 10 social platforms into an actionable toolset, now assessing 150+ partners from a variety of formats across 15 countries and establishing four new ESG-aligned priorities for partner accountability.

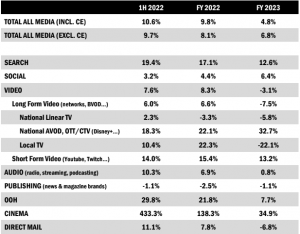

The index allows for teams and clients to incorporate brand and consumer safety priorities into their investment decision-making for a variety of media types, from the largest global social platforms to local broadcast media outlets.

The original MRI, the first-of-its kind, was launched in August 2020, in response to concerns about social media platforms not taking steps to acknowledge, measure and reduce their contribution to online and real-world harms. In effect supersized, MRI 4.0’s evaluations now encompass 80% of Mediabrands’ global investments and allow for clients to identify and invest in the media outlets that support their values without compromising ROI.

MRI 4.0 assessed each outlet across four priorities of partner accountability—Safety, Inclusivity, Sustainability and Data Ethics—in alignment with industry-adopted ESG (Environmental, Social and Governance) frameworks so businesses can easily extend how they are measuring their impact in these spaces to include media. Previous versions of the MRI had ranked the platforms upon Mediabrands’ 10 Media Responsibility Principles, which are now consolidated within the four priorities.

More than 150 major partners were surveyed, expanding into the realms of Broadcast & Cable, Connected TV, Online Video, and Display. Across Broadcast & Cable, the traditional-first networks also span several subsidiary companies across Connected TV and Online Video properties; The findings illuminated that strict, longstanding federal regulations within Broadcast & Cable have had a trickle-down effect to their digital properties, in effect enhancing safety standards when compared to digital-first counterparts surveyed.

“We developed our first media responsibility index in 2020 to determine exact protocols of the major platforms, as people started questioning the impact of social media in their lives, from the prevalence of misinformation to hate speech and data-collection practices,” said Elijah Harris, EVP Global Digital Partnerships & Media Responsibility at MAGNA. “We have always believed in the need to bring the lens of media responsibility to a broader set of media types. Consumers digest content and opinions from an ever-increasing list of mediums. It only made sense that this rigor we’ve developed for social platforms would be translated for a more diversified mix of media partners. With each iteration, the MRI is becoming more robust and establishing itself as a mainstay in driving industry accountability and powering responsible advertising investment.”

Key highlights include:

- Social media platforms showed continued improvement across the four priorities (averaging +3-point in overall performance). Partners attained a ~10% increase in Inclusivity, driven by increased focus on internal accountability and creator equity.

- Safety is a standout priority for broadcast & cable, based in part on federal industry regulations forcing uniformity and 3rd party enforcement in safety standards – including children’s safety rules and advertising approvals.

- Tech proficient digital-first CTV partners are driving higher Data Ethics performance than their traditional-first counterparts, in part due to their origins and operating in a more tech-oriented space, versus a TV-first space

- In a mixed marketplace for Sustainability practices, online video platforms showed strength in their ad-business emissions measurement + setting net-zero goals.

Advertising environments remain under the microscope as brands pursue ESG commitments and consumers become more critical of where brands choose to advertise. A Mediabrands survey found that one-quarter of clients adjusted their media mix based on MRI findings, and 90% said they were interested in finding new methods to assess media value beyond price efficiency alone.

“The MRI is an important underpinning of our Media for Good positioning, putting responsibility at the heart of every media decision, as concern over the interplay and societal impact of advertising, media and misinformation increases,” said Eileen Kiernan, Global CEO of Mediabrands. “Our clients are increasingly pursuing ESG criteria within their own businesses and we are providing a resource to support these goals along with advocating for stronger, safer standards in media.”

Examples include Snap achieving a 6-point lift YoY, outperforming all platforms in its efforts to protect people and combat misinformation and disinformation due to their robust publisher diligence; TikTok continuing to raise the bar, gaining an 8-point lift on brand safety practices and 24-point lift in children’s wellbeing; and YouTube setting the benchmark for online video across all categories, most notably in Inclusivity for delivering 60% diversity in behind the camera casting for owned and diverse content, and Safety for their policy and enforcement tools to manage UGC.

“Looking back at the strides made by social-media platforms since 2020 not only validated the need for a media responsibility monitor, it motivated us to expand the lens of media responsibility to more media types and markets,” said Harris. “We are proud to be a part of the greater journey to make social media safer for all and excited about the opportunity to improve our industry for all.”

“The 4A’s has been proud to endorse the Media Responsibility Index as an important tool for advertisers to assess how the big social-media players are handling safety issues on their platforms,” said Marla Kaplowitz, President and CEO, 4A’s. “Expanding to include other media types and global markets is a welcome next step.”

To compile MRI 4.0, MAGNA surveyed 150+ global media partners on a dynamic assessment, customized by media type, covering the most pressing safety issues of the day facing consumers and brands and specific accomplishments made by these outlets to help alleviate them. Scores were analyzed based on the varying weights of each question, as well as nuance within the individual platform, against the four brand-safety priorities.

ABOUT MEDIABRANDS:

IPG Mediabrands is the media and marketing solutions division of Interpublic Group (NYSE: IPG). Mediabrands manages approximately $40 billion in marketing investment globally on behalf of its clients and provides strategic services and solutions across its award-winning, full-service agency networks UM and Initiative and through its innovative marketing specialist companies Reprise, MAGNA, Orion, Rapport, Healix, Mediabrands Content Studio and the IPG Media Lab. Mediabrands clients include many of the world’s most recognizable and iconic brands from a broad portfolio of industry sectors. The company employs more than 13,000 marketing experts in more than 130 countries representing the full diversity of humanity. For more information, please visit our website: www.ipgmediabrands.com and be sure to follow us on LinkedIn, Twitter or Instagram.

ABOUT MAGNA:

MAGNA is the leading global media investment and intelligence company. Our trusted insights, proprietary trials offerings, industry-leading negotiation and unparalleled consultative solutions deliver an actionable marketplace advantage for our clients and subscribers. We are a team of experts driven by results, integrity and inquisitiveness. We operate across five key competencies, supporting clients and cross-functional teams through partnership, education, accountability, connectivity and enablement. For more information, please visit our website: https://magnaglobal.com/ and follow us on LinkedIn and Twitter.

PRESS CONTACT:

Isabelle Brenton

SVP, Global Corporate Communications, Mediabrands